Hearing the term financial literacy can often be intimidating, though really it is not as complicated as it seems. It is not necessarily about understanding complicated financial statements. It is simply the knowledge that we use to make financially responsible decisions; mostly to avoid over-indebtedness.

There are some typical questions that are asked in order to measure financial literacy. Usually, there is one to test knowledge about interest rates, and others to test simple calculation abilities.

During the FEDU study that was carried out in Uganda in 2016/2017, we had a special topic revolving around financial literacy. Three questions specifically show us respondents’ financial understanding and decision-making.

1. You have 5,000 UGX and you go shopping for 1 kg of sugar and 2 loaves of bread. The sugar costs 1,500 UGX and a loaf of bread costs 750 UGX each. How much change will you have?

2. If you buy 5 packets of biscuits which cost 750 UGX each, how much does that cost?

3. If you save 10,000 UGX and you leave it in the account for two years and the interest is 10% per year, how much would you have in the account after two years?

The following table shows the percentage of respondents that correctly answered each question, out of 502 respondents that were interviewed:

| Question number | % correctly answered | Male | Female |

|---|---|---|---|

| 1 | 65% (326 respondents) | 41% | 59% |

| 2 | 75.8% (380 respondents) | 44% | 56% |

| 3 | 1.2% (6 respondents) | 67% | 33% |

So clearly the questions on calculations were easier with the majority of the respondents answering correctly. Question 2 was most likely to be answered correctly, by both genders; this is a simple division problem. On the other hand, interest rates are a rather difficult topic to grasp, as is evident from the mere 1.2% that answered this question correctly (question 3).

In order to arrive at a measurement of financial literacy level, according to the above questions, we will calculate how many of the three questions were answered correctly by each respondent. That is, how many respondents had no correct answers, how many answered only one out of the three questions correctly, how many two, and how many answered all three correctly? We will define someone who answered zero questions correctly as very low, only one question correctly as having low financial literacy, two as moderate financial literacy, and those who answered all three correctly as high financial literacy.

| Number of questions answered correctly | % answered | % answered | Defined level of financial literacy | |

|---|---|---|---|---|

| Male | Female | |||

| 0.16% | (82 respondents) | 28% | 72% | Very low |

| 126% | (130 respondents) | 43% | 57% | Low |

| 257% | (288 respondents) | 42% | 58% | Moderate |

| 3.40% | (2 respondents) | 50% | 50% | High |

*Please consider rounding in the numbers above.

Only two respondents answered all three of the questions correctly.

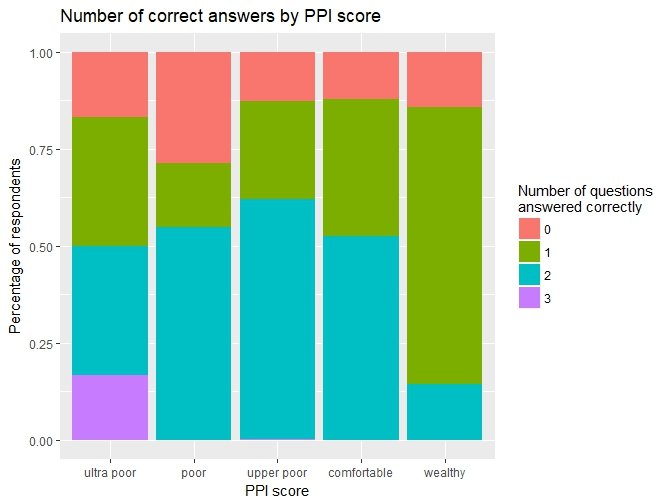

Now we wanted to investigate in our data whether higher financial literacy coincides with certain financial behavior or other dimensions we collected data on. So we asked ourselves the questions: Does this level of “financial literacy” influence people’s savings patterns? Does it have any correlation with wealth level (PPI score)? Is there a relationship between having business plans and actually implementing business ideas? And lastly, is financial literacy an influence regarding loans?

PPI score: According to a chi-square test of independence, there is indeed a relationship between PPI score and the number of questions answered correctly (i.e. level of financial literacy). We don’t know, however, which categories have this significant relationship. If we disregard the category of all 3 questions answered correctly (since there are only 2 respondents), we see that ultra-poor and poor have proportionately more respondents in the category of no questions answered correctly. The upper poor group gets proportionately bigger, and more questions are answered correctly. The comfortable have mostly answered 1 question correctly.

There is no causal relationship and no direct correlation between wealth level and financial literacy, however, there is an association.

Similarly, an analysis of variance tells us that there is a significant difference in average total income according to financial literacy level. The significant difference is between those who answered one question correctly and 2, and 1 and 3. There is no straight correlation however, we cannot say that the more financially literate have more income, for instance. The table shows the average total income over the whole 6-month research period in USD, according to the number of questions answered correctly; those who answered only one question correctly have the highest average income.

| Number of questions answered correctly | Average income | Average savings | Average net savings | Average loan | Average net loan |

|---|---|---|---|---|---|

| 0 | $142 | $51.30 | $20 | $19.80 | $-8.43 |

| 1 | $464 | $214 | $19.20 | $88.90 | $14.50 |

| 2 | $416 | $106 | $15.20 | $59.80 | $26.10 |

| 3 | $348 | $145 | $97.80 | $317 | $315 |

Savings and loans: can the level of financial literacy explain savings patterns?

Looking at savings added, there is a significant difference in the average total amount saved and financial literacy. The difference is between groups that answered 2 and 1 questions correctly, and 2 and 3. Looking at net savings (column 4), that is savings added minus withdrawn, the less financially literate, the higher the net savings. However, the test does not show a significant difference in means.

Net loans show an interesting pattern according to financial literacy level. Net loans, that is loans taken minus loans paid back (in other words, loans still outstanding) are higher the more financially literate one is. Here we see a pattern between the level of debt and level of financial literacy, though there is no statistically significant difference in means. This does not prove a causal relationship; it does not mean that the more financially literate someone is, the more debt they have. Neither does it mean that more financially literate are able to access more debt, or that inversely, more debt leads to higher financial literacy. These are all possible explanations. However, just as any of them may be at play, it may also be none of them that explain this pattern.